Inflation 2024 : Status and Prediction

Inflation 2024 : Status and Prediction

Summary of the economic and political situation

“Inflation keeps coming in hot, likely delaying interest rate cuts,” says the Washington Post headline today, and I think that’s about right.

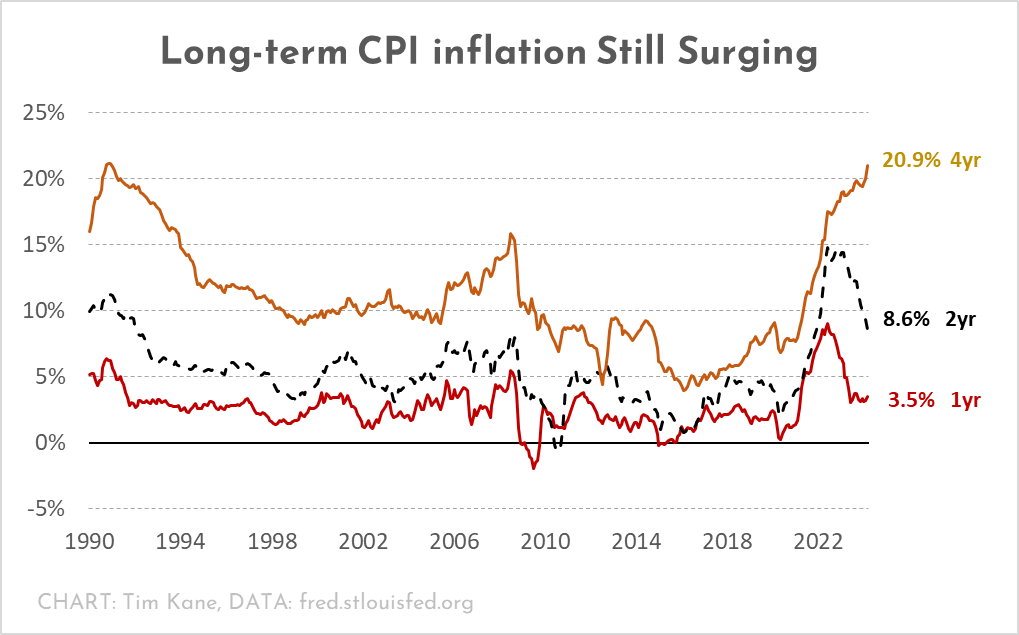

Check a hundred stories on inflation, and you will likely see the same chart of the annual inflation rate based on a yearly change in the CPI. It’s a fine chart, but I’ve come to believe that the average person thinks about inflation over a longer time horizon. To be sure, humans are sensitive to changes over a day, a month, a year, and more. We have multiple reference points, and yet the longer-term thinking is too easily neglected in conventional reporting.

Take a look at this (my) chart of 1-year, 2-year, and 4-year inflation:

Prices are 20.9% higher than they were four years ago. Nobody under the age of 40 has felt this kind of long-term price shock at any point in their lives. Indeed, most voters only felt it once, during the highly inflationary 1970s that took a decade to tame.

My second thought: How does this affect the presidential election? The fact that inflation remains “stubbornly” above 3 percent gives the Federal Reserve very little reason to lower interest rates anytime soon. The balancing act accomplished in recent years should impress you: the Fed shock-raised the FFR from zero to five hundred (basis points) in the course of a single year, then held steady. Short-term inflation was arrested without crashing GDP growth.

Take a look at this next chart. First, look at the red line spike starting in 2020 (short term inflation). Second, look at the shock-raise black line spike in 2022 (interest rates). Third, and this is the political problem, consider the sum of both lines as the pressure on citizens, especially people who want to buy a house.

Third and final thought: Is there a wage-price spiral? Seems like there is, albeit a small one. My hunch is that the reason price inflation will be hard to pull down to the conventional 2% target is that the US labor market remains strong/hot/tight, which is what you’re seeing in the jobs numbers and also the average hourly wage data. Wage growth over the past year is 4.1%, which is significantly higher than CPI inflation at 3.5%. Talk to managers and they will tell you that their employees feel a need and expectation for a hefty annual raise. That wage pressure feeds right back into price pressure, as companies have to raise prices to balance their expenses.

Do you need a recession to break that loop? I don’t think so. But you need pressure, and the FED knows it.